What Happens to Your 401(k) When You Switch Jobs—and How to Avoid Costly Mistakes

You hand in your resignation, pack up your desk, and walk out with a new job lined up. But there's one thing still sitting at your old employer: your 401(k). What you do with it in the next 60 days could either save you thousands or trigger a tax bill you never saw coming.

What you do with it in the next 60 days could either save you thousands or trigger a tax bill you never saw coming.

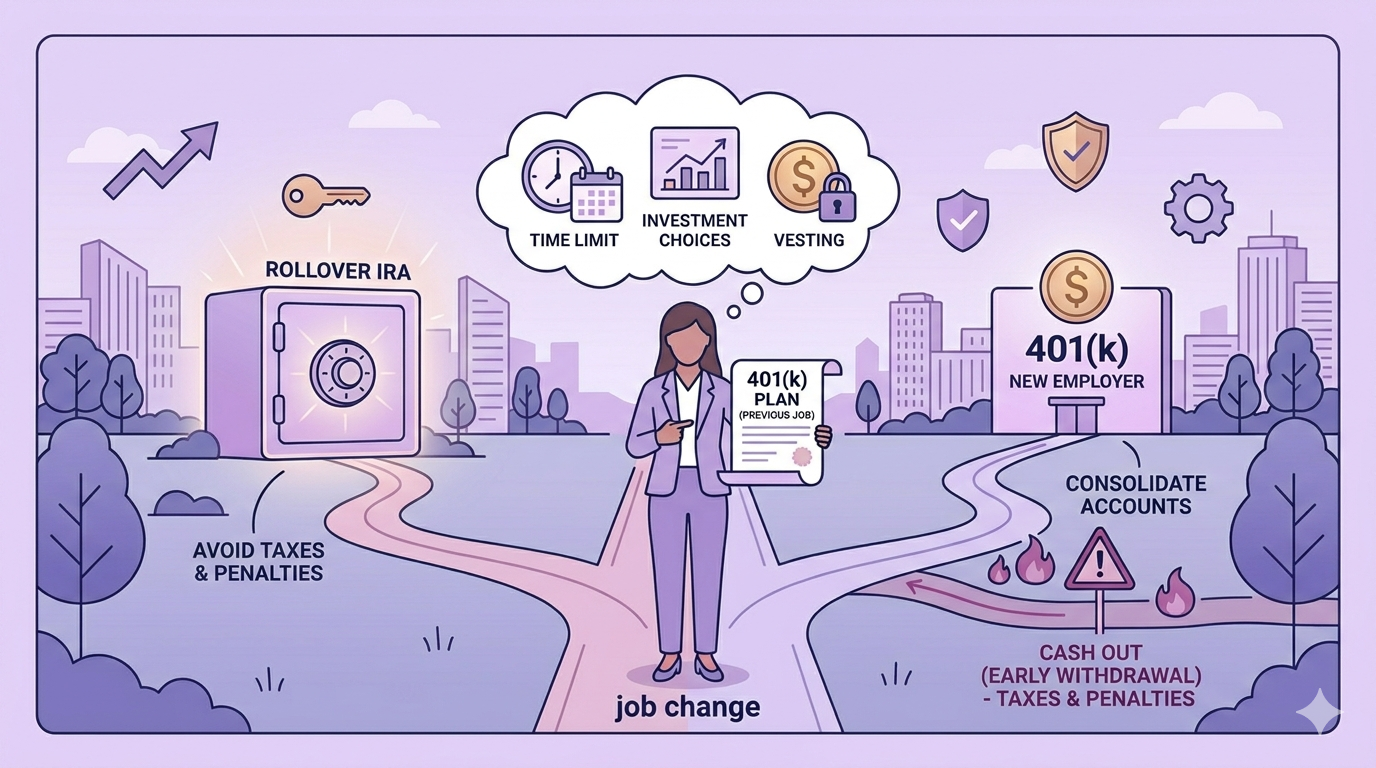

Four doors, one decision

When you leave a job, your 401(k) balance doesn't disappear—but you do have to decide what happens to it. You have four options. First, you can leave it where it is with your old employer, assuming your balance is above $5,000. Second, you can roll it into your new employer's 401(k) plan, if they accept incoming transfers. Third, you can move the money into an Individual Retirement Account, or IRA, which you open and control yourself. Fourth, you can cash it out entirely—which means paying income tax on the full amount plus a 10% early withdrawal penalty if you're under 59½. That last option is almost never worth it unless you're facing a genuine financial emergency.

The 20% withholding trap

If you decide to roll your 401(k) to a new account, how you execute the rollover matters more than most people realize. There are two types: direct and indirect. A direct rollover means the money moves straight from your old 401(k) to your new account without you ever touching it—this is the safe route. An indirect rollover means your old employer cuts you a check, and you have 60 days to deposit that money into a new retirement account.

Here's the trap: if you choose the indirect route, your old employer is required by law to withhold 20% for taxes. You'll get it back when you file your tax return, but only if you manage to deposit the full original amount—including that missing 20%—into your new account within 60 days. If you can't come up with the cash to replace the withheld portion, that chunk gets treated as a taxable distribution, and you'll owe penalties. Always request a direct rollover unless you have a specific reason not to.

Fees, funds, and future plans

So which option should you pick? It depends on a few key factors. If your old 401(k) has low fees and great investment options—think index funds with expense ratios below 0.10%—and your new employer's plan is expensive or limited, leaving it where it is might make sense. If your new employer offers a solid plan with good fund choices and low costs, consolidating everything into one account makes tracking easier.

Rolling into an IRA gives you the most control—you can invest in almost anything, and you're not stuck with whatever your employer picks—but IRAs don't have the same creditor protection as 401(k)s in every state, so if you work in a high-lawsuit-risk profession, that matters. There's also one niche consideration: if you ever want to use the backdoor Roth IRA strategy—a way high earners contribute to Roth IRAs despite income limits—having money in a traditional IRA can complicate the tax treatment. If you think you might use that strategy down the road, keeping your money in a 401(k) instead of rolling to an IRA leaves that door open.

This article is for educational purposes only and does not constitute financial advice. Always do your own research before making any investment decisions.

Curious about how a Roth IRA fits into your retirement plan? Our article on Roth vs. traditional retirement accounts breaks down the tax trade-offs in plain English.