What Is Dollar-Cost Averaging and How Does It Work?

You have $600 to invest. Do you put it all in today, or spread it across six months? Most beginners freeze at this question — terrified they'll buy at the peak. Dollar-cost averaging is the system that removes the guesswork entirely.

When prices fall, your fixed amount buys more shares. When prices rise, it buys fewer.

The mechanic behind DCA

Dollar-cost averaging — or DCA — is the practice of investing a fixed dollar amount on a regular schedule, regardless of what the market is doing. You might invest $100 every Monday, or $500 on the first of every month. The price of the stock or fund you're buying will change each time, but your contribution stays the same.

When prices fall, your fixed amount buys more shares. When prices rise, it buys fewer. Over time, this averages out your cost per share — and removes the need to guess when the market has hit bottom.

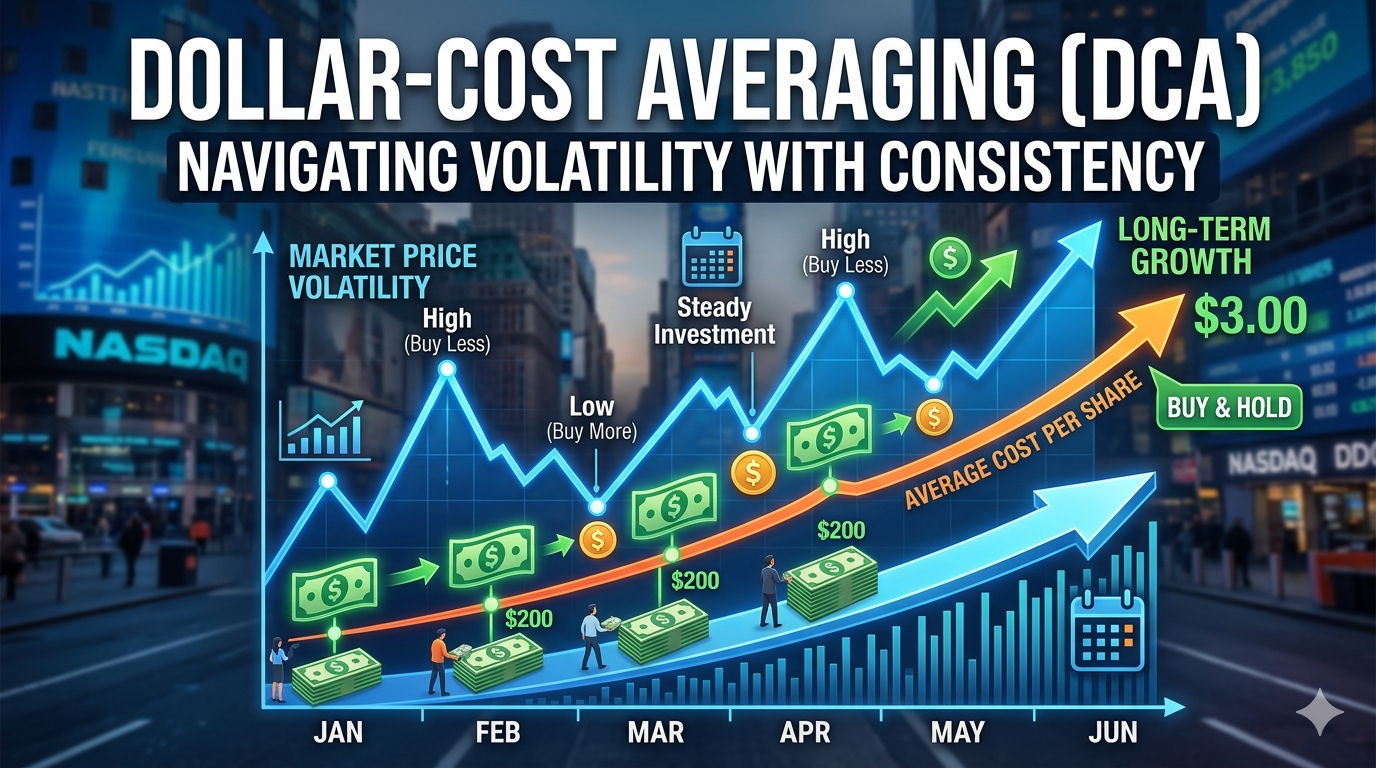

Six months, one system

Imagine you have $600 to invest in an index fund. You decide to invest $100 on the first day of each month for six months.

In January, the share price is $50, so you buy 2 shares. In February, the price drops to $40 — your $100 now buys 2.5 shares. March rebounds to $45, giving you 2.22 shares. April dips to $35, and you pick up 2.86 shares. May climbs to $48, netting 2.08 shares. June settles at $52, and you buy 1.92 shares.

You now own 13.58 shares at an average cost of $44.18. If you had invested the full $600 in January at $50 per share, you would own 12 shares and your cost per share would be $50. DCA gave you more shares at a lower average cost — without requiring you to predict which month had the best price.

What DCA does — and doesn't do

Dollar-cost averaging takes emotion out of the equation. You don't have to watch the market daily or worry that you bought at the wrong time. It also smooths out the impact of volatility — sharp swings hurt less when you're buying steadily over time.

But DCA is not a guarantee of profit, and it won't protect you from losses if the market keeps falling. If prices decline for months, your average cost will be lower than buying all at once at the start, but your position will still be underwater.

There's also a trade-off in rising markets. If prices climb steadily from the day you start, a lump sum invested up front would have beaten DCA every time — because every share you bought later cost more than it did on day one. DCA works best when you're building a position in a volatile or uncertain market, or when investing a lump sum all at once feels too risky to stomach.

This article is for educational purposes only and does not constitute financial advice. Always do your own research before making any investment decisions.

Want to see this in action? Our article on how to set up automatic investments in your brokerage account walks you through the setup step by step.